석유 충격은 생각보다 더 심각하다

The Oil Shock Is Worse Than You Think

The New York Times

Rebecca F. Elliott

EN

2026-04-10 22:32

Translated

이란과의 전쟁으로 인해 페르시아만에서 막대한 양의 석유가 흘러나오지 못하고 있지만, 많은 사람들이 추적하는 가격들은 혼란의 규모를 완전히 반영하지 못하고 있다.

구글에서 석유 가격을 검색하면 미국과 유럽에서 각각 인용되는 두 가지 광범위한 상품 가격을 찾을 수 있을 것이다.

이 가격들은 전자 시장에서 지속적으로 변하고 있으며, 이란과의 전쟁으로 인해 에너지가 훨씬 더 비싸졌지만, 상황이 4년 전 러시아가 우크라이나를 침략한 이후 만큼 나쁘지는 않다는 것을 시사한다.

하지만 실제로 석유로 가득 찬 유조선이 필요하고 신속해야 한다면, 엄청난 비용이 들 것이다.

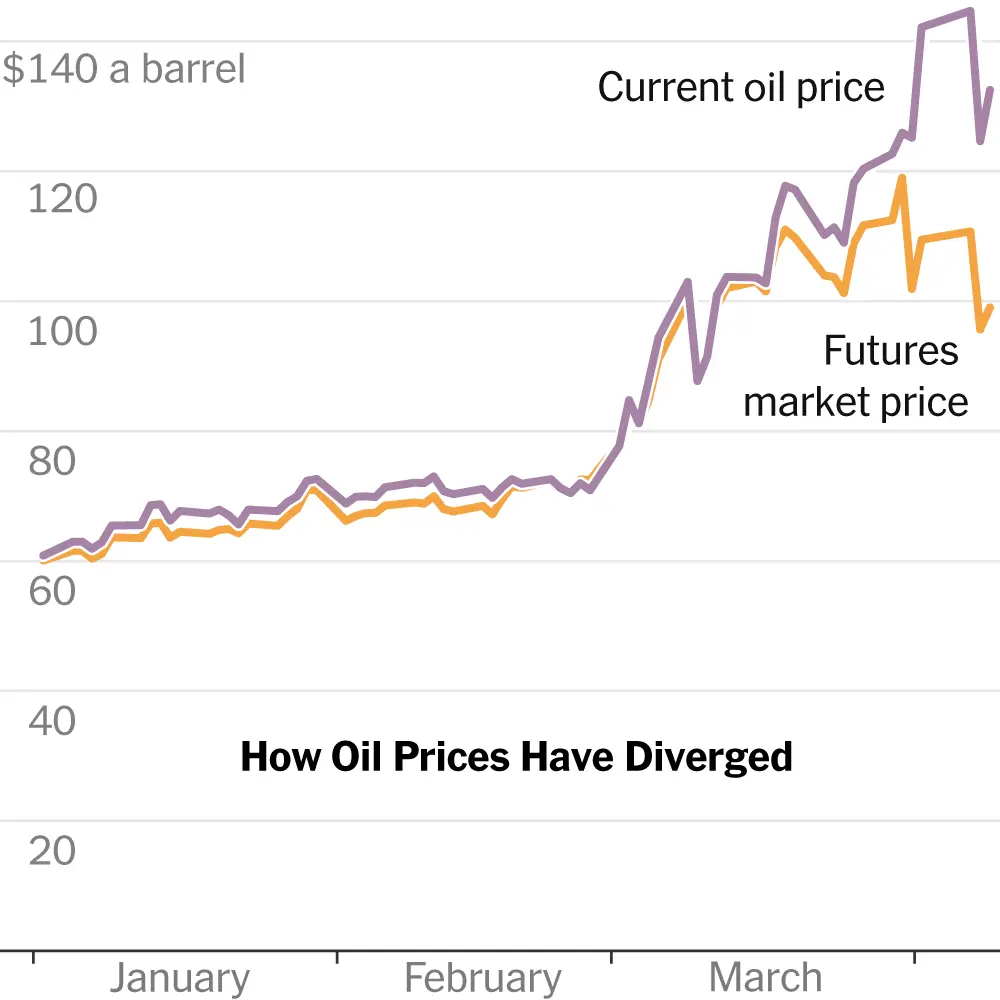

트럼프 대통령이 미국과 이란이 휴전 협정에 도달했다고 말하기 전인 화요일, 유럽의 벤트유인 일반적으로 인용되는 브렌트유 가격은 배럴당 약 109달러였다. 이는 2022년에 인플레이션을 조정하지 않고 배럴당 130달러를 넘었던 최고가보다 훨씬 낮았다.

하지만 에너지 회사들이 배에 실린 액체 석유를 사고파는 시장에서 가격은 배럴당 거의 145달러로, 상품 가격을 추적하는 회사인 Argus Media에 따르면 미국과 이스라엘이 2월 28일 이란을 공격하기 전 가격의 두 배 이상인 기록적 수준이었다.

두 가격이 그렇게 다른 이유는 첫 번째, 더 일반적으로 인용되는 가격이 선물 가격이기 때문이다. 이는 트레이더들이 1~2개월 후 석유가 얼마나 가치 있을 것으로 생각하는지를 반영하는 금융 상품이며, 가장 간단히 말해서 주가와 유사하다. 두 번째는 현물 가격이라고 불리며, 정유소가 휘발유, 디젤, 제트유로 변환할 수 있는 많은 톤의 원유 배송과 연관되어 있다.

선물 가격과 현물 가격이 정확히 같은 경우는 드물지만, 지난 몇 주 동안 그 격차가 비정상적으로 커졌으며, 석유 경영진과 분석가들은 선물 가격이 더 이상 세계가 경험하고 있는 공급 충격의 정도를 정확히 반영하지 못한다고 말하고 있다.

호주 금융 서비스 회사인 Macquarie Group의 글로벌 에너지 전략가인 Vikas Dwivedi는 "선물 시장은 지상 및 해상의 석유 현실을 전혀 반영하지 못하고 있다"고 말했다. "꽤 망가져 있다."

미국 두 번째 규모의 석유 회사인 셰브론의 최고경영자 Mike Wirth는 지난달 휴스턴 에너지 컨퍼런스인 S&P Global의 CERAWeek에서 유사한 우려를 표현했다.

"물리적 가격과 물리적 공급은 포워드 커브가 반영한다고 생각하는 것보다 더 긴축된 시장을 반영할 것이다"고 Wirth는 말했으며, 이는 선물 시장을 언급한 것이다.

현물 가격과 선물 가격은 코로나19 팬데믹과 러시아의 우크라이나 침략 같은 큰 시장 혼란 동안 종종 갈라진다. 국제적 격변은 현재의 석유 가치와 2개월 후의 가치 사이의 차이를 증폭시킨다.

하지만 최근 며칠 동안 두 가격 사이의 스프레드는 Argus 데이터에 따르면 지난 20년 동안의 다른 어떤 시기보다도 훨씬 크다. 심지어 에너지 분석가들도 이번에 그 격차가 왜 그렇게 큰지 설명하기 위해 고심했다.

"이것은 미스터리다"고 Dwivedi는 말했다.

명확한 것은 이란과의 전쟁이 석유 시장을 깊은 방식으로 뒤집어 놓았다는 것이다. 추정에 따르면, 전쟁이 시작된 이후 회사들은 호르무즈 해협(이란과 아라비아 반도 사이의 좁은 수로)을 통해 유조선을 안전하게 운송할 수 없기 때문에 세계 석유 공급의 10% 이상을 중단했다.

가격은 전 세계적으로 급등했다. 페르시아만의 연료에 크게 의존하는 아시아의 일부 국가들은 심지어 부족을 직면했다. 베트남과 태국의 주유소는 연료가 없다며 고객을 돌려보냈으며, 스리랑카는 매주 수요일을 공휴일로 선언했고, 다른 많은 국가들은 재택근무를 의무화하거나 권장했다.

이란과의 2주간의 휴전은 트럼프가 거래를 발표한 몇 시간 후 석유 가격이 급락하게 했지만, 지상에서는 거의 변한 것이 없다. 해운 회사들은 여전히 해협을 통해 선박을 보내는 것을 조심하고 있다. 이는 세계 석유의 상당 부분이 여전히 페르시아만에 갇혀 있다는 것을 의미한다.

"물리적 가격은 현재 모든 것이 얼마나 긴장되어 있는지를 알려준다"고 투자 은행 TD Cowen의 에너지 분석가 Jason Gabelman은 말했다.

이 가격들은 전자 시장에서 지속적으로 변하고 있으며, 이란과의 전쟁으로 인해 에너지가 훨씬 더 비싸졌지만, 상황이 4년 전 러시아가 우크라이나를 침략한 이후 만큼 나쁘지는 않다는 것을 시사한다.

하지만 실제로 석유로 가득 찬 유조선이 필요하고 신속해야 한다면, 엄청난 비용이 들 것이다.

트럼프 대통령이 미국과 이란이 휴전 협정에 도달했다고 말하기 전인 화요일, 유럽의 벤트유인 일반적으로 인용되는 브렌트유 가격은 배럴당 약 109달러였다. 이는 2022년에 인플레이션을 조정하지 않고 배럴당 130달러를 넘었던 최고가보다 훨씬 낮았다.

하지만 에너지 회사들이 배에 실린 액체 석유를 사고파는 시장에서 가격은 배럴당 거의 145달러로, 상품 가격을 추적하는 회사인 Argus Media에 따르면 미국과 이스라엘이 2월 28일 이란을 공격하기 전 가격의 두 배 이상인 기록적 수준이었다.

두 가격이 그렇게 다른 이유는 첫 번째, 더 일반적으로 인용되는 가격이 선물 가격이기 때문이다. 이는 트레이더들이 1~2개월 후 석유가 얼마나 가치 있을 것으로 생각하는지를 반영하는 금융 상품이며, 가장 간단히 말해서 주가와 유사하다. 두 번째는 현물 가격이라고 불리며, 정유소가 휘발유, 디젤, 제트유로 변환할 수 있는 많은 톤의 원유 배송과 연관되어 있다.

선물 가격과 현물 가격이 정확히 같은 경우는 드물지만, 지난 몇 주 동안 그 격차가 비정상적으로 커졌으며, 석유 경영진과 분석가들은 선물 가격이 더 이상 세계가 경험하고 있는 공급 충격의 정도를 정확히 반영하지 못한다고 말하고 있다.

호주 금융 서비스 회사인 Macquarie Group의 글로벌 에너지 전략가인 Vikas Dwivedi는 "선물 시장은 지상 및 해상의 석유 현실을 전혀 반영하지 못하고 있다"고 말했다. "꽤 망가져 있다."

미국 두 번째 규모의 석유 회사인 셰브론의 최고경영자 Mike Wirth는 지난달 휴스턴 에너지 컨퍼런스인 S&P Global의 CERAWeek에서 유사한 우려를 표현했다.

"물리적 가격과 물리적 공급은 포워드 커브가 반영한다고 생각하는 것보다 더 긴축된 시장을 반영할 것이다"고 Wirth는 말했으며, 이는 선물 시장을 언급한 것이다.

현물 가격과 선물 가격은 코로나19 팬데믹과 러시아의 우크라이나 침략 같은 큰 시장 혼란 동안 종종 갈라진다. 국제적 격변은 현재의 석유 가치와 2개월 후의 가치 사이의 차이를 증폭시킨다.

하지만 최근 며칠 동안 두 가격 사이의 스프레드는 Argus 데이터에 따르면 지난 20년 동안의 다른 어떤 시기보다도 훨씬 크다. 심지어 에너지 분석가들도 이번에 그 격차가 왜 그렇게 큰지 설명하기 위해 고심했다.

"이것은 미스터리다"고 Dwivedi는 말했다.

명확한 것은 이란과의 전쟁이 석유 시장을 깊은 방식으로 뒤집어 놓았다는 것이다. 추정에 따르면, 전쟁이 시작된 이후 회사들은 호르무즈 해협(이란과 아라비아 반도 사이의 좁은 수로)을 통해 유조선을 안전하게 운송할 수 없기 때문에 세계 석유 공급의 10% 이상을 중단했다.

가격은 전 세계적으로 급등했다. 페르시아만의 연료에 크게 의존하는 아시아의 일부 국가들은 심지어 부족을 직면했다. 베트남과 태국의 주유소는 연료가 없다며 고객을 돌려보냈으며, 스리랑카는 매주 수요일을 공휴일로 선언했고, 다른 많은 국가들은 재택근무를 의무화하거나 권장했다.

이란과의 2주간의 휴전은 트럼프가 거래를 발표한 몇 시간 후 석유 가격이 급락하게 했지만, 지상에서는 거의 변한 것이 없다. 해운 회사들은 여전히 해협을 통해 선박을 보내는 것을 조심하고 있다. 이는 세계 석유의 상당 부분이 여전히 페르시아만에 갇혀 있다는 것을 의미한다.

"물리적 가격은 현재 모든 것이 얼마나 긴장되어 있는지를 알려준다"고 투자 은행 TD Cowen의 에너지 분석가 Jason Gabelman은 말했다.

The war with Iran is preventing huge amounts of oil from flowing out of the Persian Gulf, but the prices that many people track don’t fully capture the scale of the disruption.

Google the price of oil, and you’ll most likely find two widely quoted prices for the commodity, one in the United States, the other in Europe.These prices, which are constantly changing on electronic markets, suggest that although the war with Iran has made energy a lot more expensive, things are not nearly as bad as they were four years ago, after Russia invaded Ukraine.

But if you needed an actual tanker full of oil — and quickly — it would cost you dearly.

On Tuesday, before President Trump said the United States and Iran had reached a cease-fire agreement, a commonly cited price of Brent oil, the European one, was about $109 a barrel. That was well below highs reached in 2022, when that price briefly topped $130, without adjusting for inflation.

But in the market where energy companies buy and sell liquid oil transported on ships, the price was almost $145 a barrel, a record and more than double the price before the United States and Israel attacked Iran on Feb. 28, according to Argus Media, a company that tracks commodity prices.

The reason the two prices were so different is that the first, more commonly cited price is the futures price. It’s a financial instrument that reflects how valuable traders think oil will be in a month or two, and — in simplest terms — is not unlike a stock price. The second is often called the spot price, and it is tied to the delivery of many tons of crude oil, which a refinery can turn into gasoline, diesel and jet fuel.

The futures and spot prices are rarely exactly the same, but the gap between them has grown unusually big in the past few weeks, so much so that oil executives and analysts say futures prices no longer accurately reflect the extent of the supply shock that the world is experiencing.

“The futures market is not representing the on-the-ground and on-the-water reality of oil at all,” said Vikas Dwivedi, global energy strategist at Macquarie Group, an Australian financial services firm. “It’s quite broken.”

Mike Wirth, the chief executive of Chevron, the second-largest U.S. oil company, expressed similar concerns last month at a Houston energy conference, CERAWeek by S&P Global.

“Physical prices and physical supplies would reflect a tighter market than I think the forward curve reflects,” Mr. Wirth said, referring to the futures market.

Spot and futures prices often diverge during big market disruptions, such as the Covid-19 pandemic and Russia’s invasion of Ukraine. International upheavals magnify the difference between the value of oil today and two months from now.

But the spread between the two prices in recent days dwarfs that of any other period in the past 20 years, Argus data show. Even energy analysts have struggled to explain why that gap is so large this time.

“It is a mystery,” Mr. Dwivedi said.

What is clear is that the war with Iran has upended oil markets in profound ways. Estimates indicate that companies have turned off 10 percent or more of the world’s oil supply since the war started because they cannot safely get tankers through the Strait of Hormuz, the narrow waterway between Iran and the Arabian Peninsula.

Prices have soared around the world. And some countries in Asia — which depends heavily on fuel from the Persian Gulf — have even faced shortages. Gas stations in Vietnam and Thailand turned away customers, saying they had no fuel; Sri Lanka declared every Wednesday a public holiday; and many other countries have mandated or encouraged remote work.

The two-week cease-fire with Iran sent oil prices plunging in the hours after Mr. Trump announced the deal, but very little has changed on the ground. Shipping companies remain wary of sending vessels through the strait. That means that a substantial portion of the world’s oil is still trapped in the Persian Gulf.

“The physical price just tells you how tight everything is right now,” said Jason Gabelman, an energy analyst at the investment bank TD Cowen.

Rebecca F. Elliott covers energy for The Times.